Download:

Abstract

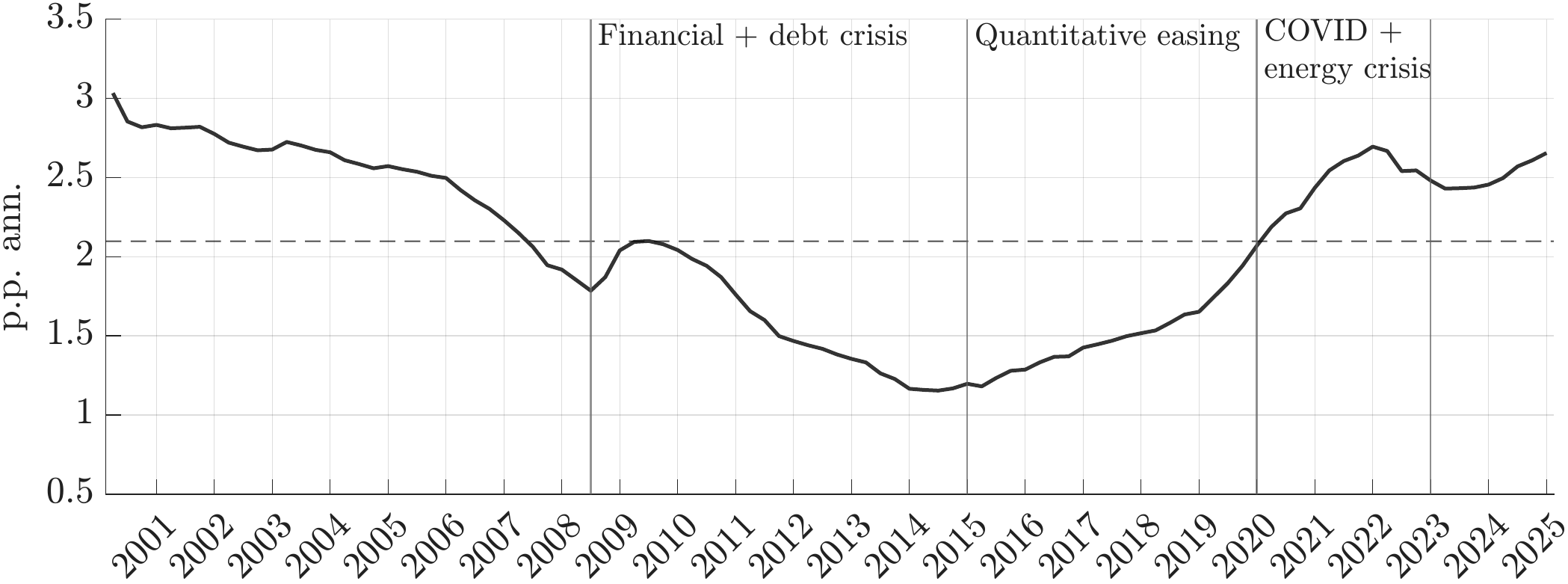

We study the propagation of unfunded fiscal shocks in a currency union. For a determinate equilibrium, at most one fiscal authority can issue unfunded debt; we then accommodate multiple partially unfunded countries by introducing monetary-led and fiscal-led parallel economies. Funded government spending shocks cause inflation to diverge across countries, while unfunded shocks raise inflation union-wide, as the common central bank accommodates fiscal inflation. Euro area local projections show that positive government spending shocks in France and Italy raise inflation at home and abroad, while in Germany they lower inflation abroad, consistent with French and Italian shocks being primarily unfunded and German shocks being primarily funded. A Bayesian-estimated quantitative model confirms that unfunded fiscal shocks are a quantitatively significant driver of euro area inflation dynamics. We recover the implied inflation target of the ECB, which averages near two percent over the sample but rose above 2.5 percent during the post-pandemic episode due to fiscal pressures.

Model implied ECB inflation target

Seminars and Presentations

2026: Bank of England, Spring Midwest Macro Meeting, Barcelona Summer Forum, Keio University, Bank of Japan

Citation:

Komatsu, M., Murakami, D. & Shchapov, I., “Fiscal Inflation in a Currency Union”. Available at SSRN: https://ssrn.com/abstract=7095239 or http://dx.doi.org/10.2139/ssrn.7095239