Download:

Abstract

A linear rational expectations model that satisfies the Blanchard-Kahn conditions is deemed as locally determinate. If this model also possesses a unique minimum state variable (MSV) solution, we term it as “globally determinate”. The canonical New Keynesian model subject to the effective lower bound (ELB) constraint does not generally possess a unique MSV solution unless monetary policy is passive; conversely violating local determinacy. This global indeterminacy problem stems from a strong feedback loop between expectations of endogenous variables and their current realisations at the ELB. This problem extends to a standard tractable heterogeneous agent New Keynesian (HANK) model. However, we show that global determinacy is restored under passive monetary policy and sufficiently limited asset market participation when “inverted aggregate demand logic” applies – further amplifying the “Catch-22 problem” in HANK models. Additionally, a standard HANK model with an active robust real rate rule fails to satisfy global determinacy conditions. But it is globally determinate with an inverted aggregate demand curve, much like the passive Taylor rule case.

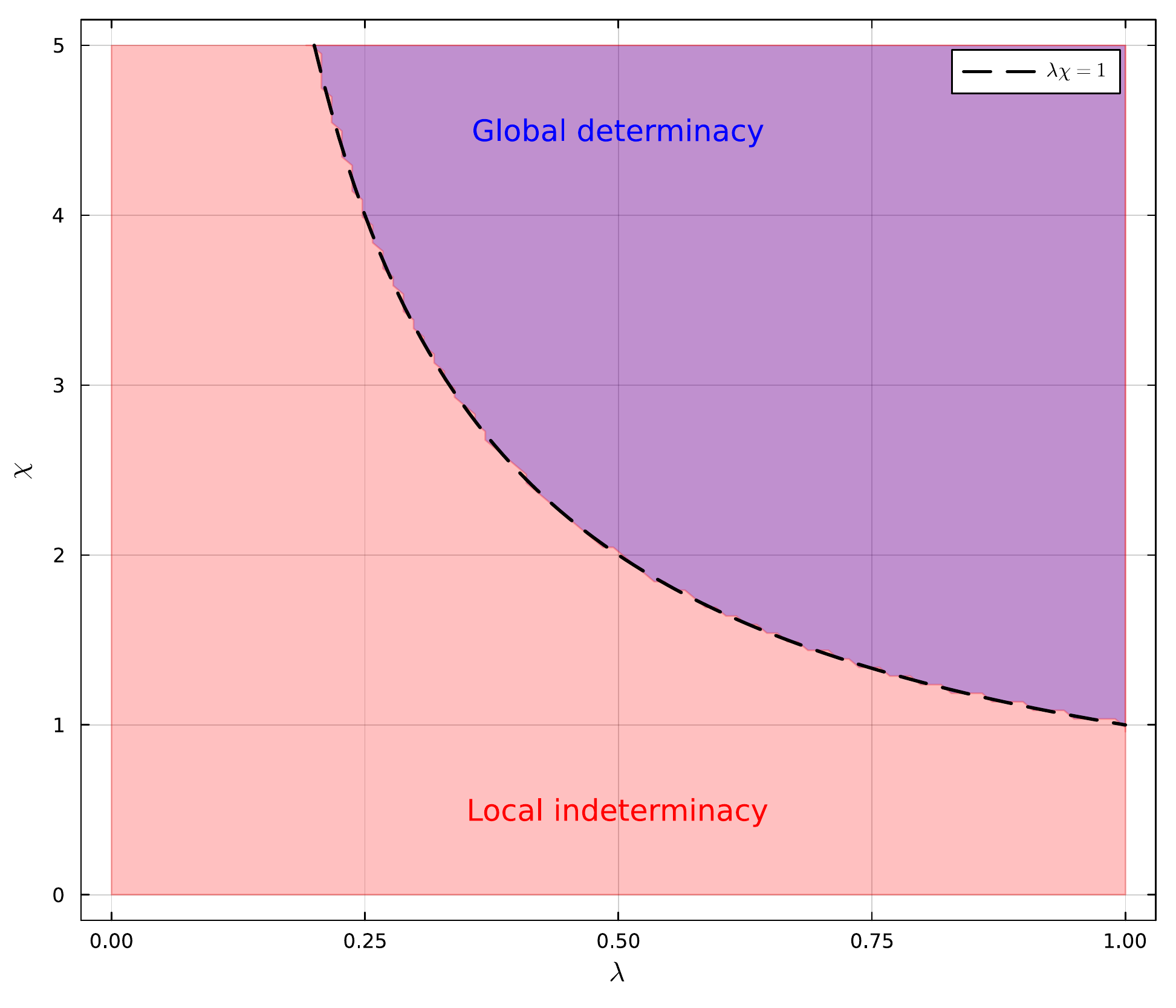

Global Determinacy Region for the HANK Model with the ELB and Taylor-Type Rule

Simulations run with $\beta=0.99$, $\sigma=2$, $\kappa = 0.1769$, $\phi=0.5$, $s=0.96$ and $p=1$. The blue region above the dashed line corresponds to inverted aggregate demand logic case ($\lambda\chi=1$), and where the model possesses global determinacy. The red region below the dashed line results in the model being locally indeterminate (Blanchard-Kahn condition violation).

Seminars and Presentations

2025: 3rd RISE Workshop (July, 2025), 5th Sailing the Macro Workshop (September, 2025), 1st WESEAMS Workshop (September, 2025)

Citation:

Murakami, David and Shchapov, Ivan and Zhang, Yifan, “Global Determinacy according to HANK” (June 20, 2025). Available at SSRN: https://ssrn.com/abstract=5314766 or http://dx.doi.org/10.2139/ssrn.5314766